How Bitcoin has served as a haven for the unbanked

- World

- May 15, 2022

Key facts:

-

Lack of education is an obstacle to financial inclusion in Latin America.

-

Unlike banks, Bitcoin is always available, regardless of date and time.

Bitcoin has been slowly occupying spaces since its launch in 2009, to the extent that traditional financial institutions and many governments, when threatened by the level of acceptance that it is gaining among the public, have tried to discredit the criptomoneda, or try to imitate it with proposals of digital currencies.

In regions such as Latin America the level of acceptance derives, among other factors, from the fact that bitcoin (BTC) it can become a lifeline for those who find themselves excluded from the financial system by the same banking which, in most cases, criticizes the cryptocurrency.

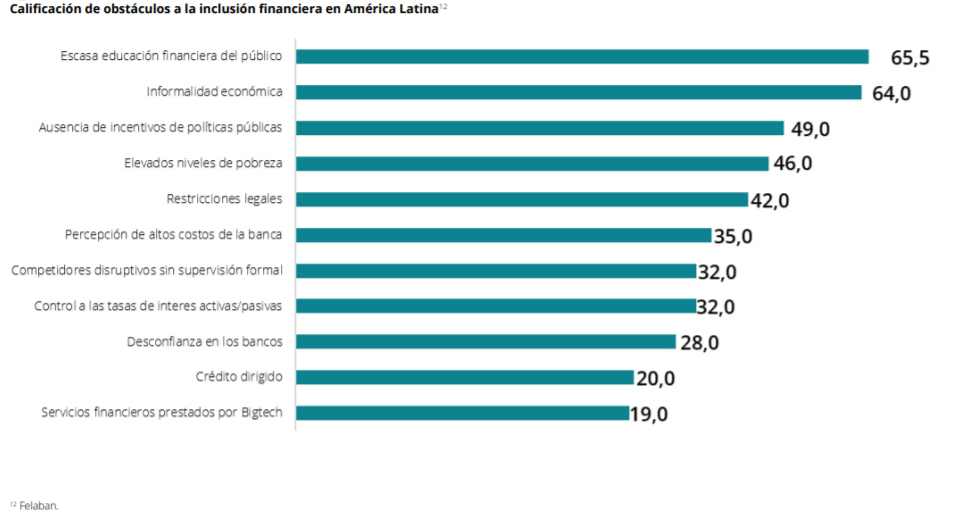

According to a study by the financial services company Deloitte, the reasons that cause financial exclusion in Latin America are poverty, informal economy, and lack of opportunities in education. This is compounded by the differentiation in the possibilities of access to credit, according to gender, in addition to the lack of infrastructure (particularly in rural areas), along with limited and deficient education.

Based on this, the analysts of this firm assure that the use of cryptocurrencies such as bitcoin would allow “to reduce transaction costs and promote financial inclusion, although in their opinion strict regulation is required, including linking with real money, and an innovative response from banks that want to remain relevant.”

However, the Deloitte study highlights that the main obstacle for new technologies to be deployed in the region is the lack of financial literacy, followed by economic informality and the absence of incentives through public policies.

It is important to note that, on the one hand, the policies of each state towards Bitcoin vary significantly. There are countries in which it is illegal, in others it is unregulated and in others it is accepted as a means of payment, for example it banned the sale of bitcoin by two banks in that country.

A case from the region that goes in the opposite direction of Argentina is that of El Salvador, the Central American country adopted bitcoin as a legal tender and promotes its use through a wallet developed by the government itself, called Chivo Wallet.

In this way, Salvadorans access cryptocurrency and learn to use it, especially those who do not have access to banking. Until 2018, only 30% of the population of El Salvador owned a bank account. Now, any Salvadoran can access goods and services by paying with bitcoin through a digital wallet.

Why is bitcoin the solution for the unbanked?

Since 2020, banks are feeling the increasing pressure of Bitcoin, for being a decentralized financial system that can separate them from the citizens. German bank Deutsche Bank pointed this out last year, stating that “cryptocurrencies increasingly pose a threat to monetary and financial stability, and central banks and governments are unlikely to give up their monetary monopolies.”

The truth is that Bitcoin could be the key for people to access free money, without censorship and without the risk of it falling into the hands of politicians. It is enough just to have a mobile phone and the internet, that is why it represents a problem for banks.

To understand this, it is important to know that Bitcoin is a peer-to-peer (P2P) electronic cash system, but it is not only about money (bills, coins or any instrument to keep accounts between people), but also about the rules and mechanisms for that cash to exist and can be used, as indicated by the Criptopedia, educational section of Criptonews.

In fact, it is such a powerful tool that, “you can say that Bitcoin, using an analogy, does the functions of the dollar, the Federal Reserve and the banking network,” all at once.

In this way, the cryptocurrency is considered as the fourth best way to manage money today. Bitcoin is a technology that combines an old financial format with new technologies. “Bitcoin allows transactions to be treated with the privacy and convenience of cash, and since it works digitally, it also adds the possibility of saving small to large sums of money and moving them to and from anywhere in the world. The best, at a low cost,” explains the Cryptopedia.

Unlike banks, funds in bitcoin can be transferred to other Bitcoin accounts, anywhere in the world 24/7/365. That is, Bitcoin has no holidays, no bosses.

Another factor that gives freedom to bitcoin users, is that each person can guard their money by themselves and transfer it without asking permission from a third party. In essence, Bitcoin does not have a “know your customer” (KYC) policy. While banks ask for a huge number of requirements (data, vouchers, references), many of them – unnecessary.

However, platforms for the sale and purchase of bitcoin have been forced to apply for KYC by pressures from bodies such as the Financial Action Task Force International (FATF), which seeks to preserve state control over money.

Something that also separates bitcoin from central banks, which are managed by small groups, which change their members depending on the president on duty, is that cryptocurrency is managed by anyone, even, the person who wants can “work” in this system, insuring it, keeping the accounts and issuing the coins.

21 million bitcoins

On the other hand, the total supply of coins in the Bitcoin system has been defined since its launch in 2009 and will reach a maximum of 21 million bitcoins in the year 2140.

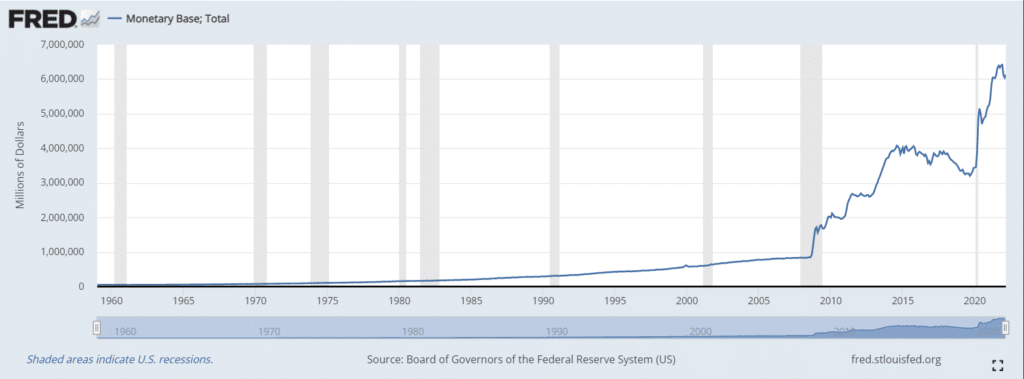

The latter contrasts with cases such as that of the United States, a country that has not stopped issuing dollars in huge quantities, especially since the beginning of the pandemic.

Until last March, the Federal Reserve (Fed) recorded an injection of money that reaches $6.3 trillion, which has had an impact on the increase in inflation, which reached a new annual record of 8.5%, the highest in 41 years.

With everything described above about Bitcoin and the different positions on cryptocurrency in countries such as Argentina and El Salvador, the digital currency created by Satoshi Nakamoto in 2009, according to the description made previously, seems to have no cracks in a banking system that is lagging behind.

The most recent rejection of a financial institution towards Bitcoin, became known when the Central African Republic adopted the cryptocurrency as legal tender. The authorities of the Central African Economic and Monetary Community (CEMAC) indicated that this was a danger for the “monetary stability” of the entire region.

Although the reality is that the unbanked who come to Bitcoin could raise their quality of life by using a system that allows them to make transactions and own their own money without having to outsource it to bank accounts they do not have, something that the authorities do not like because it escapes their control.